What strategy do domestic institutions follow – how accounts for accounts are imposed from 0.60 € to 10 € per month

By Vangelis Dourakis

“Other tricks” from domestic banking institutions, which gradually remove savings and running accounts – in substance – replacing them with young people who are “hike” from 0.60 euros to 10 euros per month: New deposit products replacing existing accounts are launched as’ privileged ‘as they enable banks’ customers to carry out a specific number Transactions without commissions.

A recent example of National Bankinforming its customers, natural persons, that the simple savings accounts, simple running and non -residents savings are gradually “upgraded” to privileges.

The “trick” of converting Savings Accounts to “Predictive”

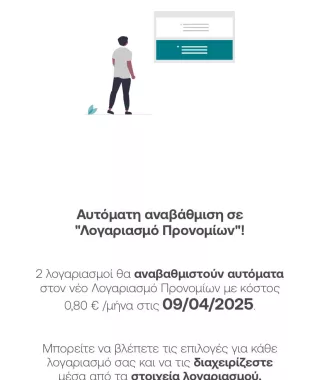

They even convert them into “privileged” is “automatically” unless the customer himself states that he does not want the procedure to proceed and express his willingness to maintain the old product. The “cheese” in order for the National Customers to accept the conversion of savings accounts and running into privileges is that With a fee of 0.80 euros per month free 4 payments per month are offeredvia Digital Banking (Internet & Mobile Banking) as well as via ATMs, free 4 fixed orders per month, free 1 outbound internal transfer to euro up to 5,000 euros per month and free 1 inbound internal transfer at up to € 5,000 per month!

This move might have made the meaning of “bid” before mid -January, when and from the invoices of the four systemic groups, it emerged that the cost of payments only to the fixed costs of a family or business (electricity, water, water, water, water, water, water, water, water, Phone, etc.) ranged from 0.15 euros to 1.20 euros per transaction via e-banking, which made such a bank proposal Properly without a “second conversation”.

However, the data has changed, as a number of commissions have been abolished after government intervention, and in particular adopted:

- Zero charge for paying bills and debts to the State, insurance funds, local government agencies and other general government bodies, decentralized administrations, electricity, gas, water, telecommunications and insurance companies, Mobile – Banking. The cost until recently was € 0.60 per transaction.

- Maximum billing of 0.5 euros for sending money (outgoing remittance) and 0.5 euros for money (incoming transfer), for amounts of up to 5,000 euros per remittance, for natural persons and freelancers, between banks in Greece, which cost 2.5 to 5 euros.

In other words, every bank’s customer should “weigh” if it is really advantageous to accept its accession to the new “privileged” accounts, since several supplies imposed on daily transactions have already been … abolished.

Financial institutions, however A series of transactions!

Which banks offer ‘privileged’ accounts with… charge

The National Bank, however Eurobankwhich had decided to allocate to its customers – existing, but also new – four subscription packages (My Advantage Blue – Silver – Gold – Platinum), accompanied by a “package” of service from 0.60 euros to 10 euros per euro per month.

The monthly commission for the basic program, which is 0.60 euros, provides, inter alia, keeping billing, free debit card and prepaid card, free fixed orders to pay accounts to all organizations, free account payments online based on Article 48 of N of .5167/2024 and free transfers up to 500 euros a day from the Eurobank Mobile App with the Iris Payments service.

On her side the Alpha Bank, It has the Myalpha Benefit range for a cost of 3 euros and 5 euros a month: if one chooses the “package” of 3 euros free money transfers up to 5,000 euros, debit and credit without subscription and up to 3 withdrawals from other banks at no charge. If he chooses the expensive “package” of 5 “earns” unlimited money transfer up to 5,000 euros and unlimited cash withdrawals from other banks and of course debit and credit without subscription.

OR Piraeus Bank It had the repayment order where the annual subscription was 10 or 25 euros and was based on the logic of inexpensive redemption of all accounts, either through a standing order, or electronically via winbank, or through stores, with a maximum of 50 free transactions per year. This “package” at this time seems disabled as it will be “upgraded”.

What changes in the strategy of domestic banks

In any case, domestic banking institutions seem to impose … by side, constant monthly bank account costs on all their customers.

After all, next time they will have to differentiate their strategy in order to get revenue, as we also go into an environmental reduction environment: In previous years banks have exploited high interest rates and their excessive liquidity as they found themselves with billions of deposits. who did not transform into loans and which they placed in the ECB reaping And risk, hundreds of millions of euros giving a great boost to their profitability.

With the reduction of interest rates, these … “skyscrapers” revenue will be limited, making it doubtful to maintain their profitability at 2024 levels.

So the key to their profitability in the coming years is to expand the sources of revenue from new fields: and one of them is supplies.

In addition, by the gradual conversion of all savings accounts into “privileged” with a constant monthly charge, in addition to creating a new source of income from supplies, it is estimated that they will reduce operating costs from maintaining forgotten or double and triple accounts without balances.

Source: Skai

I am Janice Wiggins, and I am an author at News Bulletin 247, and I mostly cover economy news. I have a lot of experience in this field, and I know how to get the information that people need. I am a very reliable source, and I always make sure that my readers can trust me.