According to analysts, the extended boom period that began during the COVID era is over, as after the surge in demand for microchips during the pandemic, which led to large shortages in the market, the situation has reversed

With a negative sign of 9%, the global semiconductor market closed in 2023, the revenue of which decreased for the first time, after a two-year strong upward trend. The global semiconductor industry last year recorded revenues of $545 billion from an estimated $598 billion in 2022.

“This decline follows two years of record growth, highlighting the cyclical nature of the semiconductor market. Now, demand has softened due to macroeconomic factors, while the supply of semiconductor components has increased,” says Omdia’s latest “Competitive Landscape Tool” report.

The global microchip market will reach $545 billion in 2023, recording a decline after a two-year rise

According to analysts, the extended boom period that began during the COVID era is over, as after the surge in demand for microchips during the pandemic, which led to large shortages in the market, the situation has reversed.

According to Omdia’s analysis, the memory market saw a decline in 2023 overall, while the HBM market recorded strong growth of 127% year-on-year in terms of 1Gb equivalent units throughout 2023.

Omdia predicts that the HBM market is likely to record higher unit growth rates in 2024, ranging between 150%-200% and is expected to drive the growth of the memory market.

It should be noted that in 2023 the automotive industry was also the protagonist of the demand for microchips, with the increase of electric vehicles and the integration of AI in cars driving the demand for semiconductors from the sector.

The winners of AI

Despite declining demand and an overall decline in the microchip market in 2023, the industry was not short of bright spots, with artificial intelligence emerging as a major growth driver for the semiconductor industry.

Unsurprisingly, companies focused on this segment of the market, related to artificial intelligence, were the big winners. “THE NVIDIA was the clear winner in this area, more than doubling its semiconductor revenue from 2022 to $49 billion in 2023. This achievement demonstrates its leap forward NVIDIAas its semiconductor revenue was below $10 billion before the pandemic in 2019,” analysts say.

NVIDIA, however, was not the only player in the semiconductor market to benefit from the rise of artificial intelligence. High-bandwidth memory (HBM), integrated with GPUs to facilitate artificial intelligence, is also in high demand, with SK Hynix leading the way and other major memory manufacturers venturing into this space.

The protagonists

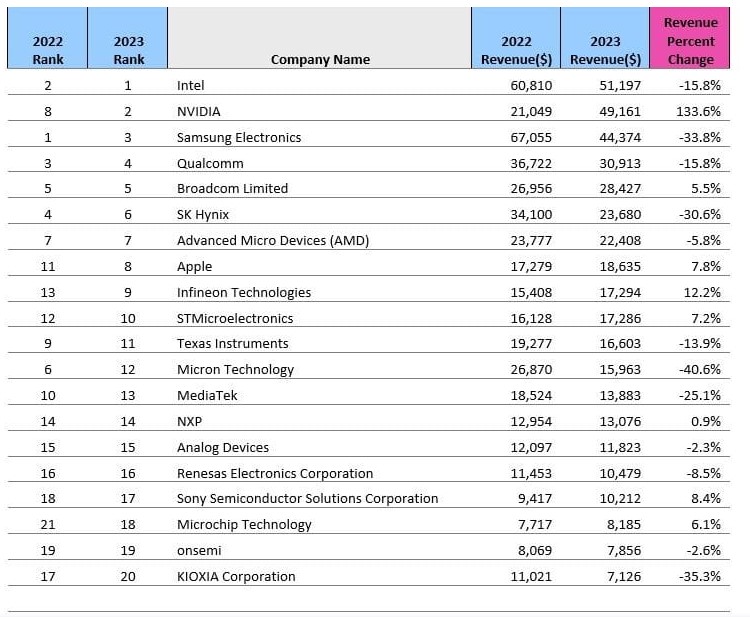

In terms of players in the global microchip industry, according to Omdia’s analysis, Intel maintains the top ranking – in terms of revenue – with NVIDIA following as the second largest semiconductor company by revenue in 2023. Samsung, leader of industry in 2022, fell to third place in 2023 as memory revenue nearly halved from 2021 levels.

“The recession hit the big memory manufacturers hard. From 2017 to 2021, the Samsung Electronicsthe SK Hynix and the Microns Technology ranked in the top five of the global market by revenue. However, in the difficult conditions of the memory market, the Samsung Electronics is now ranked third, h SK Hynix in the sixth and n Microns Technology in the twelfth”, concludes Omdia.

Source :Skai

I am Terrance Carlson, author at News Bulletin 247. I mostly cover technology news and I have been working in this field for a long time. I have a lot of experience and I am highly knowledgeable in this area. I am a very reliable source of information and I always make sure to provide accurate news to my readers.